|

IATA's global passenger traffic results

for May 2018 show that demand (measured in revenue passenger

kilometers, or RPKs) rose 6.1% compared to the same month in 2017,

which was a slight pickup from 6.0% year-over-year growth for

April 2018.

Capacity climbed 5.9% and load factor rose 0.1

percentage point to 80.1%.

"May was another solid month in

terms of demand growth. As had been expected, we saw some

moderation, as rising airline costs are reducing the stimulus from

lower airfares. In particular, jet fuel prices are expected to be

up nearly 26% this year compared to 2017. Nevertheless, the record

load factor for the month signifies that demand for air

connectivity is strong," said Alexandre de Juniac, IATA�s Director

General and CEO.

International passenger traffic demand rose 5.8%, which was up

from 4.6% growth in April. All regions recorded growth, led by

Asia- Pacific airlines. Total capacity climbed 5.4%, with load

factor rising 0.3 percentage point to 78.7%.

Asia-Pacific

airlines saw their traffic rise 8.0% in May compared to the

year-ago period, slightly down on an 8.1% increase in April.

Capacity increased 7.6%, and load factor edged up 0.3 percentages

point to 77.9%. Passenger traffic has continued to trend strongly

upwards in seasonally-adjusted terms, buoyed by a combination of

robust regional economic growth and increases in the number of route options for travelers.

European carriers� May

demand climbed 6.2% over May 2017, well above the 3.4%

year-over-year growth recorded in April. Capacity rose 5.1% and

load factor was up 0.8 percentage point to 83.5%, which was the

highest among regions. Despite the impact of strikes in the region

and mixed signals regarding the economic backdrop, traffic growth

is healthy.

Middle East carriers� May demand growth

slowed to 0.8% compared to a year ago, from 2.9% annual growth

recorded in April. The earlier timing of Ramadan this year may

have affected the result, but more broadly, the upward trend in

traffic has slowed compared to last year. May capacity increased

3.7%, and load factor fell 1.9 percentage points to 67.5%.

North American airlines� traffic rose 4.9% in May

compared to May 2017, a strong rebound from 0.9% annual growth in

April (which was a 36-month low). Capacity climbed 3.4% and load

factor increased 1.2 percentage points to 82.0%. Given the

comparatively strong US domestic economy, April�s weak demand

performance likely was more reflective of unfavorable year-to-year comparisons with April 2017, when the current upsurge in growth

began.

Latin American airlines experienced a 7.5%

increase in traffic in May compared to the same month last year,

which was up from 6.5% growth in April. Capacity climbed 7.0% and

load factor rose 0.4 percentage points to 81.6%. Economic

disruption in Brazil may be contributing to a slight slowdown in

demand growth in recent months, but this is not expected to have a

long-term impact on the healthy traffic trend.

African airlines� traffic rose 3.8% in May compared to the

year-ago period, which was an 8-month low. Capacity rose 3.2% and

load factor edged up 0.4 percentage point to 66.4%. The region�s

two largest economies, Nigeria and South Africa, may be moving in opposite directions again, with higher oil prices bolstering the

Nigerian economy, while business confidence in South Africa has weakened again.

Domestic Passenger Markets

Domestic

demand rose 6.6% in May compared to May 2017, led by growth in

China and India. This was down from the 8.6% year-on-year growth

recorded in April largely owing to moderate growth in both

countries, although each continued to post double-digit traffic

gains.

India�s domestic traffic rose 16.6%

year-over-year, which was down from 25.7% in April. Passenger

volumes in India have fallen back in seasonally-adjusted terms in

recent months alongside some mixed signals on the economic front.

Notwithstanding this, May was India�s 45th consecutive month of

double-digit annual RPK growth. Demand continues to be supported

by strong growth in the number of airport connections within the

country: some 22% more airport-pairs are scheduled to operate in

2018 compared to last year.

US domestic traffic

experienced a mild pick-up in May, with 5.5% year-over-year

traffic growth, up from 5.3% in April. This partly offset the

moderate growth in China and India. Domestic traffic is trending

upward at an annualized rate of around 7%, helped by the

comparatively strong US economy.

"Last month, IATA released its mid-year economic report showing

expectations of an industry net profit of $33.8 billion. This is a

solid performance. But our buffer against shocks is just $7.76.

That�s the average profit per passenger that airlines will make

this year�a narrow 4.1% net margin. And there are storm clouds on

the horizon, including rising cost inputs, growing protectionist

sentiment and the risk of trade wars, as well as geopolitical

tensions. Aviation is the business of freedom, liberating people

to lead better lives. Governments that recognize this will take

steps to ensure aviation is economically sustainable. And aviation

works best when borders are open to trade and people," said de

Juniac.

See latest

HD Video

Interviews,

Podcasts

and other

news regarding:

IATA,

Aviation,

Traffic.

|

Mandarin Oriental Opens Special Hotel in Beijing, China

Mandarin Oriental Opens Special Hotel in Beijing, China AirAsia to Launch Penang - Shenzhen and Kota Kinabalu - Shantou Flights

AirAsia to Launch Penang - Shenzhen and Kota Kinabalu - Shantou Flights Boeing Forecasts Passenger and Cargo Needs of China's Aviation Industry

Boeing Forecasts Passenger and Cargo Needs of China's Aviation Industry Air Corsica Takes Delivery of ATR's 1,700th Turboprop Aircraft

Air Corsica Takes Delivery of ATR's 1,700th Turboprop Aircraft Minor Hotels to Open Anantara Resort Ubud Bali in October

Minor Hotels to Open Anantara Resort Ubud Bali in October Uruguayan Air Force to Add A-29 Super Tucano Aircraft to Fleet

Uruguayan Air Force to Add A-29 Super Tucano Aircraft to Fleet Air Astana to Increase Flights to Phuket, Thailand; Signs Codeshare Deal with JAL

Air Astana to Increase Flights to Phuket, Thailand; Signs Codeshare Deal with JAL Hong Kong Airlines to Resume Long-Haul Flights with Seasonal Gold Coast Service

Hong Kong Airlines to Resume Long-Haul Flights with Seasonal Gold Coast Service IHG Signs Two Hotels in Quang Binh, Vietnam

IHG Signs Two Hotels in Quang Binh, Vietnam Marriott Opens Moxy Hotel in Mumbai, India

Marriott Opens Moxy Hotel in Mumbai, India Torsten Richter Returns to Minor Hotels as AGM of Indonesia and Malaysia

Torsten Richter Returns to Minor Hotels as AGM of Indonesia and Malaysia Minor Set to Open World's Third NH Resort in Maldives

Minor Set to Open World's Third NH Resort in Maldives Asiana Airlines and Air Serbia Appoint APG as GSA

Asiana Airlines and Air Serbia Appoint APG as GSA IndiGo to Launch New Delhi - Vijayawada Flights

IndiGo to Launch New Delhi - Vijayawada Flights Hong Kong Airport Reports Strong Increases in Cargo and Passenger Traffic

Hong Kong Airport Reports Strong Increases in Cargo and Passenger Traffic Delta Begins Rollout of Free Wi-Fi on Long-Haul International Routes

Delta Begins Rollout of Free Wi-Fi on Long-Haul International Routes Thai AirAsia X to Resume Flights Between Bangkok and Sydney, Australia

Thai AirAsia X to Resume Flights Between Bangkok and Sydney, Australia Marriott Partners Sonder to Add Over 9,000 Rooms to Portfolio

Marriott Partners Sonder to Add Over 9,000 Rooms to Portfolio IHG Opens Hotel Indigo in Bandung, Indonesia

IHG Opens Hotel Indigo in Bandung, Indonesia IndiGo Enhances Operations with Aviobook, an Electronic Flight Folder from Thales

IndiGo Enhances Operations with Aviobook, an Electronic Flight Folder from Thales Boeing Invests in Wagner SAF Refinery in Brisbane, Australia

Boeing Invests in Wagner SAF Refinery in Brisbane, Australia Aeroflot to Resume Flights Between Yekaterinburg and Bangkok, Phuket and Goa

Aeroflot to Resume Flights Between Yekaterinburg and Bangkok, Phuket and Goa Air Astana Takes Delivery of 56th Aircraft; Confirms Plan to Launch Phu Quoc Flights

Air Astana Takes Delivery of 56th Aircraft; Confirms Plan to Launch Phu Quoc Flights Seibu Prince Rebrands Hotel in Singapore

Seibu Prince Rebrands Hotel in Singapore airBaltic Appoints APG as GSA in Egypt

airBaltic Appoints APG as GSA in Egypt Korean Air and Delta Air Lines Partner Habitat for Humanity to Make a Difference in Cheonan

Korean Air and Delta Air Lines Partner Habitat for Humanity to Make a Difference in Cheonan Air New Zealand, Garuda, Qantas and Singapore Airlines Begin UPR Trials on 38 Routes

Air New Zealand, Garuda, Qantas and Singapore Airlines Begin UPR Trials on 38 Routes Thai AirAsia Reports Q2 and H1 2024 Results; Confirms Full-Year Targets

Thai AirAsia Reports Q2 and H1 2024 Results; Confirms Full-Year Targets EL AL Israel Airlines Finalises Deal for 31 Aircraft

EL AL Israel Airlines Finalises Deal for 31 Aircraft Cebu Pacific to Launch Davao - Hong Kong and Iloilo - Singapore Flights

Cebu Pacific to Launch Davao - Hong Kong and Iloilo - Singapore Flights Poland to Become Largest Operator of Apache Combat Helicopters Outside of USA

Poland to Become Largest Operator of Apache Combat Helicopters Outside of USA Singha Estate Partners Ascott for Rebranding of Two Hotels in the United Kingdom

Singha Estate Partners Ascott for Rebranding of Two Hotels in the United Kingdom IndiGo to Launch Coimbatore - Singapore Flights; Increase Frequency of Select Services

IndiGo to Launch Coimbatore - Singapore Flights; Increase Frequency of Select Services Parveen Kumar Joins Grand Hyatt Jakarta as General Manager

Parveen Kumar Joins Grand Hyatt Jakarta as General Manager Azerai Appoints Jimmy Tran as Group Director of Sales & Marketing

Azerai Appoints Jimmy Tran as Group Director of Sales & Marketing South Korea to Strengthen Airborne Surveillance and Reconnaissance Capabilities

South Korea to Strengthen Airborne Surveillance and Reconnaissance Capabilities Virgin Australia to Replace Fokker 100s with Embraer E190-E2 Aircraft

Virgin Australia to Replace Fokker 100s with Embraer E190-E2 Aircraft Cross Adds Two Hotels in Bangkok, Thailand to Portfolio

Cross Adds Two Hotels in Bangkok, Thailand to Portfolio airBaltic Exercises Options on 10 Airbus A220-300 Aircraft

airBaltic Exercises Options on 10 Airbus A220-300 Aircraft Etihad to Increase Thailand Flights; Resume A380 Service to Singapore

Etihad to Increase Thailand Flights; Resume A380 Service to Singapore Dusit Signs Hotel and Condo on Rama 3 Road in Bangkok, Thailand

Dusit Signs Hotel and Condo on Rama 3 Road in Bangkok, Thailand Cape and Kantary Hotels to Expand Portfolio with Serviced Suites in Korat, Thailand

Cape and Kantary Hotels to Expand Portfolio with Serviced Suites in Korat, Thailand Thai Airways Reports Q2 and H1 2024 Results

Thai Airways Reports Q2 and H1 2024 Results China Airlines Extends Cargo Handling Contract with FCS

China Airlines Extends Cargo Handling Contract with FCS Goldfinch Becomes First Piloted Electric Aircraft to Fly at NASA's Langley Research Center

Goldfinch Becomes First Piloted Electric Aircraft to Fly at NASA's Langley Research Center Rosewood Signs Luxury 33-Suite Resort in Exuma, Bahamas

Rosewood Signs Luxury 33-Suite Resort in Exuma, Bahamas British Airways Expands Codeshare with Bangkok Airways

British Airways Expands Codeshare with Bangkok Airways Aeroflot Unveils Most Popular International Destinations in H1 2024

Aeroflot Unveils Most Popular International Destinations in H1 2024 Marriott Executive Apartments Open on Sukhumvit Soi 49 in Bangkok, Thailand

Marriott Executive Apartments Open on Sukhumvit Soi 49 in Bangkok, Thailand Uday Rao Appointed RVP and GM of Four Seasons Hotel Tokyo at Otemachi in Japan

Uday Rao Appointed RVP and GM of Four Seasons Hotel Tokyo at Otemachi in Japan CapitaLand Ascott Trust Secures OCBC 1.5°C Loan

CapitaLand Ascott Trust Secures OCBC 1.5°C Loan Sabre Hospitality Enhances SynXis Booking Engine with Trip Protection Services

Sabre Hospitality Enhances SynXis Booking Engine with Trip Protection Services Cathay Pacific Orders 30 Airbus A330-900 Aircraft

Cathay Pacific Orders 30 Airbus A330-900 Aircraft Haytham Said Appointed GM of Four Seasons Hotel Miami

Haytham Said Appointed GM of Four Seasons Hotel Miami Hong Kong Airport Launches World's First Smartphone Express Bag Drop Service

Hong Kong Airport Launches World's First Smartphone Express Bag Drop Service Marriott Signs W Hotel in Hangzhou, China

Marriott Signs W Hotel in Hangzhou, China IndiGo Selects Recaro's R2 and R5 Seats for New A321neo Aircraft

IndiGo Selects Recaro's R2 and R5 Seats for New A321neo Aircraft Scoot to Take Delivery of Jalan-Jalan and Travel Kaki E190-E2s in September and October

Scoot to Take Delivery of Jalan-Jalan and Travel Kaki E190-E2s in September and October Ali Mohammed Appointed Regional Vice President and GM of Four Seasons Resort Orlando

Ali Mohammed Appointed Regional Vice President and GM of Four Seasons Resort Orlando Marriott Opens Fourth Executive Apartments Property in Bangkok, Thailand

Marriott Opens Fourth Executive Apartments Property in Bangkok, Thailand AirAsia X to Resume Kuala Lumpur - Chongqing Flights

AirAsia X to Resume Kuala Lumpur - Chongqing Flights Norse Operates Non-Stop Charter Flight from Oslo to Darwin, Australia

Norse Operates Non-Stop Charter Flight from Oslo to Darwin, Australia Wyndham Reports Record H1 Growth in Asia Pacific

Wyndham Reports Record H1 Growth in Asia Pacific LOT Polish Airlines Takes Delivery of First Embraer E195-E2

LOT Polish Airlines Takes Delivery of First Embraer E195-E2 Vietnam Airlines Takes Delivery of Fifth Boeing 787-10 Aircraft

Vietnam Airlines Takes Delivery of Fifth Boeing 787-10 Aircraft Marriott Expands Executive Apartments Brand to Penang, Malaysia

Marriott Expands Executive Apartments Brand to Penang, Malaysia AirAsia Group Expands Fleet with Four Airbus A321neo Aircraft

AirAsia Group Expands Fleet with Four Airbus A321neo Aircraft IATA Reports Latest Airline Passenger Traffic Data

IATA Reports Latest Airline Passenger Traffic Data China Airlines Signs SAF-Related MOU with Morrison Express

China Airlines Signs SAF-Related MOU with Morrison Express Fairfield by Marriott Hotel Opens in Terengganu, Malaysia

Fairfield by Marriott Hotel Opens in Terengganu, Malaysia IATA Reports Latest Global Air Cargo Data

IATA Reports Latest Global Air Cargo Data Marriott Opens Fifth Autograph Collection Hotel in Japan

Marriott Opens Fifth Autograph Collection Hotel in Japan Matthew Smith to Succeed Monique Arnoux as CEO of Destination Asia

Matthew Smith to Succeed Monique Arnoux as CEO of Destination Asia American Airlines Renews Subscription to Prism

American Airlines Renews Subscription to Prism Shanghai Pudong Airport Installs 52 Kiosks and 14 Self-Service Bag Drops from SITA

Shanghai Pudong Airport Installs 52 Kiosks and 14 Self-Service Bag Drops from SITA Hong Kong Airport Handled 4.3 Million Passengers and 29,590 Flight Movements in June

Hong Kong Airport Handled 4.3 Million Passengers and 29,590 Flight Movements in June Croatia Airlines Takes Delivery of First Airbus A220

Croatia Airlines Takes Delivery of First Airbus A220 Ryanair to Implement Boeing's Jeppesen FliteDeck Pro 5.0 EFB

Ryanair to Implement Boeing's Jeppesen FliteDeck Pro 5.0 EFB Asia Pacific Airlines Carried 28.9 Million International Passengers in June

Asia Pacific Airlines Carried 28.9 Million International Passengers in June Singapore Changi Airport Reports Q2 2024 Traffic

Singapore Changi Airport Reports Q2 2024 Traffic Cat Wu Returns to Singapore as Executive Director of Revenue for Two Hotels

Cat Wu Returns to Singapore as Executive Director of Revenue for Two Hotels Langham Appoints Jack Xiao as Senior Vice President of Operations - China

Langham Appoints Jack Xiao as Senior Vice President of Operations - China NATO Selects Sikorsky X2 Rotorcraft for Integrated Platform Concept Study

NATO Selects Sikorsky X2 Rotorcraft for Integrated Platform Concept Study Malaysia Airlines Expands Retailing Strategy with NDC Content on Travelport

Malaysia Airlines Expands Retailing Strategy with NDC Content on Travelport Air Tahiti Orders Four ATR 72-600 Aircraft

Air Tahiti Orders Four ATR 72-600 Aircraft One Air to Expand Fleet with Third Boeing 747-400 Freighter

One Air to Expand Fleet with Third Boeing 747-400 Freighter FCM Travel Expands Cytric Distribution Agreement with Amadeus

FCM Travel Expands Cytric Distribution Agreement with Amadeus Cathay Pacific Expands 1 Ticket, 1 Tree Initiative to Include Cargo

Cathay Pacific Expands 1 Ticket, 1 Tree Initiative to Include Cargo Japan Airlines Confirms Order for 20 Airbus A350-900s and 11 A321neos

Japan Airlines Confirms Order for 20 Airbus A350-900s and 11 A321neos Embraer E190 Freighter Receives ANAC Type Certification

Embraer E190 Freighter Receives ANAC Type Certification Libya's Berniq Airways Orders Six A320neo Family Aircraft

Libya's Berniq Airways Orders Six A320neo Family Aircraft Qatar Airways Adds 20 Boeing 777-9s to Order Book

Qatar Airways Adds 20 Boeing 777-9s to Order Book Accor Signs Raffles Hotel in Tokyo, Japan

Accor Signs Raffles Hotel in Tokyo, Japan Thai AirAsia to Launch Bangkok - Hyderabad and Phuket - Siem Reap Flights

Thai AirAsia to Launch Bangkok - Hyderabad and Phuket - Siem Reap Flights Courtyard by Marriott Hotel Opens in Sapporo, Japan

Courtyard by Marriott Hotel Opens in Sapporo, Japan Qatar Airways Unveils Qsuite Next Gen at Farnborough Airshow 2024

Qatar Airways Unveils Qsuite Next Gen at Farnborough Airshow 2024 British Airways Increases Number of Funded Places in Speedbird Pilot Academy

British Airways Increases Number of Funded Places in Speedbird Pilot Academy Mandarin Oriental Signs Hotel and Residences in Bali, Indonesia

Mandarin Oriental Signs Hotel and Residences in Bali, Indonesia Minor Hotels Signs Dual-Branded Property in Yining, China

Minor Hotels Signs Dual-Branded Property in Yining, China Korean Air Takes Delivery of First Boeing 787-10 Dreamliner

Korean Air Takes Delivery of First Boeing 787-10 Dreamliner Two Senior Promotions at IHG Asia Pacific

Two Senior Promotions at IHG Asia Pacific Miss International Queen 2024 (MIQ 2024) - Interview with Alisa Phanthusak, MD, Tiffany's Show Pattaya, Thailand

Miss International Queen 2024 (MIQ 2024) - Interview with Alisa Phanthusak, MD, Tiffany's Show Pattaya, Thailand Airbus A321XLR Powered by CFM LEAP-1A Engines Receives EASA Type Certification

Airbus A321XLR Powered by CFM LEAP-1A Engines Receives EASA Type Certification New Dusit Thani Bangkok Hotel to Open 27 September 2024

New Dusit Thani Bangkok Hotel to Open 27 September 2024 CWT Upgrades Airfare Optimization Service with AI and Machine Learning

CWT Upgrades Airfare Optimization Service with AI and Machine Learning Small Luxury Hotels of the World Returns to India with MRS Group Partnership

Small Luxury Hotels of the World Returns to India with MRS Group Partnership SATS and SF Group Sign MOU to Expand Global Footprint

SATS and SF Group Sign MOU to Expand Global Footprint Thai AirAsia to Launch Don Mueang - Lampang Flights

Thai AirAsia to Launch Don Mueang - Lampang Flights Hong Kong Welcomed 3.13 Million Visitor Arrivals in June 2024

Hong Kong Welcomed 3.13 Million Visitor Arrivals in June 2024 China Airlines Launches Direct Flights Between Taipei and Seattle, USA

China Airlines Launches Direct Flights Between Taipei and Seattle, USA London Heathrow Airport Expands Partnership with SITA

London Heathrow Airport Expands Partnership with SITA bp Partners Audi Formula 1 Team

bp Partners Audi Formula 1 Team Qantas Launches Non-Stop Flights Between Perth and Paris, France

Qantas Launches Non-Stop Flights Between Perth and Paris, France Marriott Signs First Ritz-Carlton Reserve in UAE

Marriott Signs First Ritz-Carlton Reserve in UAE Vietnam Airlines to Launch Flights Between Hanoi and Phnom Penh, Cambodia

Vietnam Airlines to Launch Flights Between Hanoi and Phnom Penh, Cambodia Saudia and flyadeal Increase Flights to Abha; Group Reports Positive H1 Numbers

Saudia and flyadeal Increase Flights to Abha; Group Reports Positive H1 Numbers SITA Completes Legal and Regulatory Formalities for Materna IPS Acquisition

SITA Completes Legal and Regulatory Formalities for Materna IPS Acquisition Marriott Opens AC Hotel in Gunpo City, South Korea

Marriott Opens AC Hotel in Gunpo City, South Korea Air France-KLM Signs Codeshare and Interline Agreements with Scandinavian Airlines

Air France-KLM Signs Codeshare and Interline Agreements with Scandinavian Airlines IHG Signs Four Hotels in Spain

IHG Signs Four Hotels in Spain Entries Open for 2025 New Zealand Millennium Cup Regatta

Entries Open for 2025 New Zealand Millennium Cup Regatta American Airlines to Develop Aviation Maintenance Talent Pipeline with Tulsa Tech

American Airlines to Develop Aviation Maintenance Talent Pipeline with Tulsa Tech IHG Signs First Vignette Collection Hotel in Almaty, Kazakhstan

IHG Signs First Vignette Collection Hotel in Almaty, Kazakhstan Hahnair Partners German Formula 1 Driver, Nico Hülkenberg

Hahnair Partners German Formula 1 Driver, Nico Hülkenberg Travelport Enhances Platform with AI and ML-Powered Content Curation Layer

Travelport Enhances Platform with AI and ML-Powered Content Curation Layer Cotai Water Jet to Launch Macau Fireworks and Sightseeing Cruises

Cotai Water Jet to Launch Macau Fireworks and Sightseeing Cruises United Airlines Applies to Launch New Daily DCA - SFO Service

United Airlines Applies to Launch New Daily DCA - SFO Service Luminara, a Ritz-Carlton SuperYacht, to Cruise Asia Pacific in 2025-26

Luminara, a Ritz-Carlton SuperYacht, to Cruise Asia Pacific in 2025-26 Afrijet Appoints APG as GSA in South Africa

Afrijet Appoints APG as GSA in South Africa Euros 2024 a Record-Breaking Success for Hotels in Cologne, Germany

Euros 2024 a Record-Breaking Success for Hotels in Cologne, Germany Etihad Airways to Increase Flights to Boston, USA; Operate A350 on Toronto Service

Etihad Airways to Increase Flights to Boston, USA; Operate A350 on Toronto Service Saudi Arabia Orders Four A330 Multi Role Tanker Transport Aircraft from Airbus

Saudi Arabia Orders Four A330 Multi Role Tanker Transport Aircraft from Airbus Ascott Becomes Official Global Hotels Partner of Chelsea FC; Will Take Over Stadium Hotels

Ascott Becomes Official Global Hotels Partner of Chelsea FC; Will Take Over Stadium Hotels Indochina Kajima Gets Green Light for Construction of Mandarin Oriental Bai Nom in Vietnam

Indochina Kajima Gets Green Light for Construction of Mandarin Oriental Bai Nom in Vietnam Rahul Dangwal Joins Amora Riverwalk Melbourne; Rob Unson Joins Amora Brisbane

Rahul Dangwal Joins Amora Riverwalk Melbourne; Rob Unson Joins Amora Brisbane Air Canada Signs Deal for Eight Boeing 737-8 Aircraft

Air Canada Signs Deal for Eight Boeing 737-8 Aircraft Cebu Pacific Takes Delivery of 7th Aircraft of the Year

Cebu Pacific Takes Delivery of 7th Aircraft of the Year SITA Reports Record Results; Future of Air Travel - Podcast and Video Interview with Sumesh Patel, President of SITA Asia Pacific

SITA Reports Record Results; Future of Air Travel - Podcast and Video Interview with Sumesh Patel, President of SITA Asia Pacific Vietnam Airlines Takes Delivery of First Airbus A320neo

Vietnam Airlines Takes Delivery of First Airbus A320neo Marriott Opens 100th Sheraton Hotel in Greater China

Marriott Opens 100th Sheraton Hotel in Greater China Syahreza Ishwara Appointed GM of Anantara Koh Yao Yai Resort & Villas in Thailand

Syahreza Ishwara Appointed GM of Anantara Koh Yao Yai Resort & Villas in Thailand Tiong Nam Hospitality Adds Marina in Puteri Harbour, Malaysia to Portfolio

Tiong Nam Hospitality Adds Marina in Puteri Harbour, Malaysia to Portfolio Sabah Tourism Board Signs 5-Year Agreement with AirAsia

Sabah Tourism Board Signs 5-Year Agreement with AirAsia Turkish Airlines to Expand Cargo Fleet with Four Boeing 777 Freighters

Turkish Airlines to Expand Cargo Fleet with Four Boeing 777 Freighters Zurich Airport to Trial Security Solutions from Smiths Detection

Zurich Airport to Trial Security Solutions from Smiths Detection IATA Reports Global Air Cargo Data for May 2024

IATA Reports Global Air Cargo Data for May 2024 AirAsia Launches KL - Sihanoukville Flights; Confirms KL - Labuan Bajo Service

AirAsia Launches KL - Sihanoukville Flights; Confirms KL - Labuan Bajo Service Inaugural Tourism Seasonality Summit to Take Place at Routes World 2024 in Bahrain

Inaugural Tourism Seasonality Summit to Take Place at Routes World 2024 in Bahrain Hahnair Adds 10 Airlines to HR-169 Ticket Solution

Hahnair Adds 10 Airlines to HR-169 Ticket Solution WFS Opens Fifth Cargo Terminal at Adolfo Suarez Madrid-Barajas Airport in Spain

WFS Opens Fifth Cargo Terminal at Adolfo Suarez Madrid-Barajas Airport in Spain Four Senior Appointments at New Dusit Thani Bangkok Hotel

Four Senior Appointments at New Dusit Thani Bangkok Hotel Onyx Opens First Shama Hotel and Serviced Apartments in Malaysia

Onyx Opens First Shama Hotel and Serviced Apartments in Malaysia IHG Signs First Hotel in Kashmir

IHG Signs First Hotel in Kashmir World's Largest Aloft Hotel Appoints Tan Kim Seng as General Manager

World's Largest Aloft Hotel Appoints Tan Kim Seng as General Manager AirAsia X to Launch Flights Between Kuala Lumpur and Nairobi, Kenya

AirAsia X to Launch Flights Between Kuala Lumpur and Nairobi, Kenya Minor Signs Deal to Rebrand Peace Resort Samui as NH Collection Samui

Minor Signs Deal to Rebrand Peace Resort Samui as NH Collection Samui Thai Airways Resumes Flights to Milan and Oslo

Thai Airways Resumes Flights to Milan and Oslo Kylie Minogue to Perform at Mandarin Oriental Bodrum's 10th Anniversary Party

Kylie Minogue to Perform at Mandarin Oriental Bodrum's 10th Anniversary Party Eve Air Mobility Raises US$94 Million in New Equity Financing

Eve Air Mobility Raises US$94 Million in New Equity Financing Thai AirAsia Launches Suvarnabhumi - Hat Yai Flights

Thai AirAsia Launches Suvarnabhumi - Hat Yai Flights Jesper Larsen Returns to Vietnam as GM of InterContinental Halong Bay Resort and Residences

Jesper Larsen Returns to Vietnam as GM of InterContinental Halong Bay Resort and Residences Six Key Appointments at Ascott

Six Key Appointments at Ascott Finnair Completes Long-Haul Cabin Renewal

Finnair Completes Long-Haul Cabin Renewal AirAsia to Launch Flights Between Kuala Lumpur and Chiang Rai, Thailand

AirAsia to Launch Flights Between Kuala Lumpur and Chiang Rai, Thailand Thai Airways Expands Partnership with Amadeus

Thai Airways Expands Partnership with Amadeus Asia Pacific Airlines Carried 27.9 Million International Passengers in May

Asia Pacific Airlines Carried 27.9 Million International Passengers in May Korean Air Cargo Expands SAF Program with CEVA Logistics Partnership

Korean Air Cargo Expands SAF Program with CEVA Logistics Partnership IHG Signs First Holiday Inn Express Hotel in Egypt

IHG Signs First Holiday Inn Express Hotel in Egypt Ticket Booking Opens for World Travel Market 2024 in London

Ticket Booking Opens for World Travel Market 2024 in London Spotnana Enhances Service with Sabre's NDC Content

Spotnana Enhances Service with Sabre's NDC Content Codeshare Flights Between Kuwait and Thai Airways Take Off

Codeshare Flights Between Kuwait and Thai Airways Take Off Singapore Airlines Extends Cargo Handling Contracts with WFS

Singapore Airlines Extends Cargo Handling Contracts with WFS Courtyard by Marriott Hotel Opens Near Colva Beach in Goa, India

Courtyard by Marriott Hotel Opens Near Colva Beach in Goa, India Air Mauritius Joins AirAsia Move OTA

Air Mauritius Joins AirAsia Move OTA LOT Polish Airlines Appoints APG as Online GSA in Saudi Arabia

LOT Polish Airlines Appoints APG as Online GSA in Saudi Arabia Onyx Hospitality Expands Shama Hub Brand to Hangzhou and Hong Kong

Onyx Hospitality Expands Shama Hub Brand to Hangzhou and Hong Kong Minor to Take Over Management of Iconic Hotel in Bangkok, Thailand

Minor to Take Over Management of Iconic Hotel in Bangkok, Thailand Singapore Airlines to Launch Flights to Beijing Daxing; Increase Beijing Capital Service

Singapore Airlines to Launch Flights to Beijing Daxing; Increase Beijing Capital Service Marriott Opens Fourth Courtyard Hotel in Malaysia

Marriott Opens Fourth Courtyard Hotel in Malaysia Momentus Hospitality Appoints Chow Keng Hai as General Manager

Momentus Hospitality Appoints Chow Keng Hai as General Manager Helicopter Designed for French Special Forces Begins Flight Tests

Helicopter Designed for French Special Forces Begins Flight Tests Westin Resort Opens in Cam Ranh, Vietnam

Westin Resort Opens in Cam Ranh, Vietnam Google Wallet Compatibility Added to Vingcard's Digital Key Solution, Mobile Access

Google Wallet Compatibility Added to Vingcard's Digital Key Solution, Mobile Access Cross Signs New-Build Resort on Batam Island in Indonesia

Cross Signs New-Build Resort on Batam Island in Indonesia Korean Air Increasing Select Flights to China and Japan

Korean Air Increasing Select Flights to China and Japan Air Astana Donates Upcycled Aircraft Furniture to Almaty Airport

Air Astana Donates Upcycled Aircraft Furniture to Almaty Airport Jetstar Asia Resumes Flights Between Singapore and Clark, Philippines

Jetstar Asia Resumes Flights Between Singapore and Clark, Philippines Sabre Hospitality to Showcase SynXis Concierge.AI at HITEC 2024

Sabre Hospitality to Showcase SynXis Concierge.AI at HITEC 2024 St. Regis Resort Opens in Al Mouj, Oman

St. Regis Resort Opens in Al Mouj, Oman Percy Muncherji and Ron Cusiter Join Thailand's Centara Hotels and Resorts

Percy Muncherji and Ron Cusiter Join Thailand's Centara Hotels and Resorts Four Seasons Yachts Unveils Details of More Voyages Planned for 2026

Four Seasons Yachts Unveils Details of More Voyages Planned for 2026 Sabre to Upgrade Sun Siyam Resorts' Distribution and Retailing Strategy

Sabre to Upgrade Sun Siyam Resorts' Distribution and Retailing Strategy Positive Outlook as Asia Pacific Airlines Return to Profitability

Positive Outlook as Asia Pacific Airlines Return to Profitability SITA Reports Continued Reduction in Mishandled Baggage by Air Transport Industry

SITA Reports Continued Reduction in Mishandled Baggage by Air Transport Industry Scandinavian Airlines Launches Daily Flights Between Copenhagen and Atlanta, USA

Scandinavian Airlines Launches Daily Flights Between Copenhagen and Atlanta, USA Belgium Orders 17 Airbus H145M Helicopters

Belgium Orders 17 Airbus H145M Helicopters AirAsia Resumes Direct Flights Between Kuala Lumpur and Pattaya, Thailand

AirAsia Resumes Direct Flights Between Kuala Lumpur and Pattaya, Thailand Vietnam Airlines Launches Flights Between Saigon and Manila, Philippines

Vietnam Airlines Launches Flights Between Saigon and Manila, Philippines Korean Air Selects Air Incheon as Preferred Bidder for Asiana's Freighter Business

Korean Air Selects Air Incheon as Preferred Bidder for Asiana's Freighter Business Marriott to Significantly Expand Portfolio of Hotels in France

Marriott to Significantly Expand Portfolio of Hotels in France Avianca Resumes Eleven International Routes

Avianca Resumes Eleven International Routes IHG Signs First Kimpton Resort in Hawaii

IHG Signs First Kimpton Resort in Hawaii Laurence Neumann Joins Gran Melia Nha Trang as DOSM

Laurence Neumann Joins Gran Melia Nha Trang as DOSM Frasers Hospitality Expands Sabre Partnership with SynXis Retailing

Frasers Hospitality Expands Sabre Partnership with SynXis Retailing IHG Signs Holiday Inn Resort in Kufri, India

IHG Signs Holiday Inn Resort in Kufri, India Charles Szar Joins AeroTransCargo as President

Charles Szar Joins AeroTransCargo as President Saudi Arabia's Travel and Tourism Sector Continues to Break Records

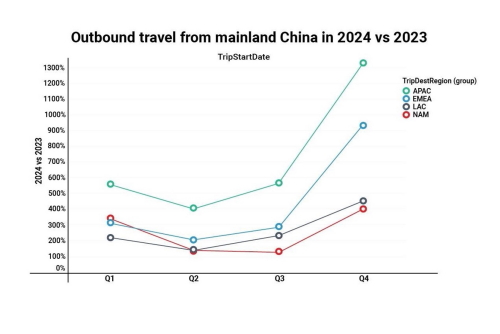

Saudi Arabia's Travel and Tourism Sector Continues to Break Records Sabre Market Intelligence Reveals Key Insights into China's Outbound Travel Trends

Sabre Market Intelligence Reveals Key Insights into China's Outbound Travel Trends Geoff Donaghy, CEO of ICC Sydney, Resigns

Geoff Donaghy, CEO of ICC Sydney, Resigns Emirates to Launch Dubai - Seychelles - Madagascar Flights

Emirates to Launch Dubai - Seychelles - Madagascar Flights Pan Pacific Returns to Jakarta with Tallest Luxury Hotel in the City

Pan Pacific Returns to Jakarta with Tallest Luxury Hotel in the City Saudia and Virgin Atlantic Sign Codeshare Agreement

Saudia and Virgin Atlantic Sign Codeshare Agreement SalamAir to Launch Flights Between Muscat and Delhi, India

SalamAir to Launch Flights Between Muscat and Delhi, India Radisson to Expand Red Hotel Brand to Bangkok, Thailand

Radisson to Expand Red Hotel Brand to Bangkok, Thailand Plaza Premium Expands Number of Personalised Services at Hong Kong Airport

Plaza Premium Expands Number of Personalised Services at Hong Kong Airport Vietnam Airlines Joins IATA CO2 Connect

Vietnam Airlines Joins IATA CO2 Connect Dusit Signs Dual-Branded Hotel and Residences in Phuket, Thailand

Dusit Signs Dual-Branded Hotel and Residences in Phuket, Thailand Hong Kong Airlines to Launch Flights to Da Nang, Vietnam

Hong Kong Airlines to Launch Flights to Da Nang, Vietnam Singapore University Working with SITA to Upgrade Air Travel Experience

Singapore University Working with SITA to Upgrade Air Travel Experience Germany Orders 38 Airbus H225 Helicopters for Bundespolizei

Germany Orders 38 Airbus H225 Helicopters for Bundespolizei AI to Reduce Food Waste at All Mandarin Oriental Hotels Globally

AI to Reduce Food Waste at All Mandarin Oriental Hotels Globally ITA Airways to Upgrade Network Infrastructure with SITA Connect Go

ITA Airways to Upgrade Network Infrastructure with SITA Connect Go Accor to Implement Amadeus' Cloud-Based Central Reservation System

Accor to Implement Amadeus' Cloud-Based Central Reservation System Gonzalo Aguilar to Join Minor Hotels as CEO - Europe & Americas

Gonzalo Aguilar to Join Minor Hotels as CEO - Europe & Americas Cathay Pacific and Singapore Airlines to Collaborate on Sustainable Initiatives

Cathay Pacific and Singapore Airlines to Collaborate on Sustainable Initiatives Minor Takes Over Management of Two Hotels in Sri Lanka

Minor Takes Over Management of Two Hotels in Sri Lanka CapitaLand Completes Acquisition of Standard at Columbia Student Accommodation in USA

CapitaLand Completes Acquisition of Standard at Columbia Student Accommodation in USA Singapore Airlines Renews Slot and Schedule Manager Agreement with Sabre

Singapore Airlines Renews Slot and Schedule Manager Agreement with Sabre Austrian Airlines to Increase Flights to Bangkok, Thailand

Austrian Airlines to Increase Flights to Bangkok, Thailand Riyadh Air and Singapore Airlines to Explore Interline Connectivity and More

Riyadh Air and Singapore Airlines to Explore Interline Connectivity and More Mandarin Oriental Opens Second Hotel in London, England

Mandarin Oriental Opens Second Hotel in London, England Mexicana Orders 20 Embraer E2 Aircraft

Mexicana Orders 20 Embraer E2 Aircraft Lufthansa Launches Flights Between Munich and Seattle, USA

Lufthansa Launches Flights Between Munich and Seattle, USA Airbus to Showcase Wingman Concept at ILA Berlin

Airbus to Showcase Wingman Concept at ILA Berlin Marriott Resort Opens in Lampung, Indonesia

Marriott Resort Opens in Lampung, Indonesia IndiGo and Japan Airlines Agree to Codeshare

IndiGo and Japan Airlines Agree to Codeshare Ritz-Carlton Reserve Opens on Ummahat Island in Saudi Arabia

Ritz-Carlton Reserve Opens on Ummahat Island in Saudi Arabia Norse Atlantic Airways Launches Flights Between Athens and New York, USA

Norse Atlantic Airways Launches Flights Between Athens and New York, USA British Airways Opens Refurbished Lounge at Lagos Airport in Nigeria

British Airways Opens Refurbished Lounge at Lagos Airport in Nigeria Hong Kong Airport Reports Robust Increases in Passenger and Cargo Traffic

Hong Kong Airport Reports Robust Increases in Passenger and Cargo Traffic Marriott Opens Luxury Collection Resort in Labuan Bajo, Indonesia

Marriott Opens Luxury Collection Resort in Labuan Bajo, Indonesia Dusit Expands Senior Development Team with Two Executive Appointments

Dusit Expands Senior Development Team with Two Executive Appointments Hong Kong Airlines to Launch Flights to Taichung, Taiwan

Hong Kong Airlines to Launch Flights to Taichung, Taiwan Aviation: RPK Up 11%, ASK Up 9.6 and PLF at 82.4% in April 2024

Aviation: RPK Up 11%, ASK Up 9.6 and PLF at 82.4% in April 2024 Furama to Rebrand Hotel in Sydney, Australia

Furama to Rebrand Hotel in Sydney, Australia IHG Signs Two Crowne Plaza Hotels in Egypt

IHG Signs Two Crowne Plaza Hotels in Egypt IATA Reports Latest Air Cargo Data

IATA Reports Latest Air Cargo Data Air Canada Expands Ottawa Network

Air Canada Expands Ottawa Network Marriott Signs Tribute Portfolio Hotels in Chongqing, Jiande and Xiaoshan, China

Marriott Signs Tribute Portfolio Hotels in Chongqing, Jiande and Xiaoshan, China Keishi Spa Swan Valley Relocates to Novotel Perth Murray Street in Australia

Keishi Spa Swan Valley Relocates to Novotel Perth Murray Street in Australia Korean Air's Afforestation Project in Baganuur, Mongolia Celebrates 20th Anniversary

Korean Air's Afforestation Project in Baganuur, Mongolia Celebrates 20th Anniversary Etihad Airways Becomes Main Sponsor of Girona FC

Etihad Airways Becomes Main Sponsor of Girona FC Rolls-Royce Adds Airline Support Baltic to Network of Authorised Service Centers

Rolls-Royce Adds Airline Support Baltic to Network of Authorised Service Centers Radisson Signs Blu Resort in Ho Tram, Vietnam

Radisson Signs Blu Resort in Ho Tram, Vietnam Treamprom Klinhom Joins Moxy Bangkok Ratchaprasong as MarCom Manager

Treamprom Klinhom Joins Moxy Bangkok Ratchaprasong as MarCom Manager The Slate Phuket Launches Promotion for Thai Residents

The Slate Phuket Launches Promotion for Thai Residents Airbus to Establish Tech Hub in Japan

Airbus to Establish Tech Hub in Japan Sabre Embraces Increasing Power of AI to Launch SabreMosaic

Sabre Embraces Increasing Power of AI to Launch SabreMosaic Thailand International Boat Show to Take Place at Phuket Yacht Haven in 2025

Thailand International Boat Show to Take Place at Phuket Yacht Haven in 2025 Aeroflot Opens Ticket Sales on Flights Between Krasnoyarsk and Sanya, China

Aeroflot Opens Ticket Sales on Flights Between Krasnoyarsk and Sanya, China Norwegian Cruise Line Unveils Details of 24 Port-Intensive Cruises Across Asia

Norwegian Cruise Line Unveils Details of 24 Port-Intensive Cruises Across Asia British Airways to Launch Seasonal Flights to Tromsø, Norway

British Airways to Launch Seasonal Flights to Tromsø, Norway SITA Expands Portfolio of Airport Solutions with Materna IPS Acquisition

SITA Expands Portfolio of Airport Solutions with Materna IPS Acquisition United Airlines Takes Wrexham AFC's Recent Success to New Heights

United Airlines Takes Wrexham AFC's Recent Success to New Heights Peter Tichy Joins Radisson Blu Plaza Bangkok as General Manager

Peter Tichy Joins Radisson Blu Plaza Bangkok as General Manager SMFL LCI Orders 14 Airbus Helicopters

SMFL LCI Orders 14 Airbus Helicopters Apollo Extends Charter Contract with Scandinavian Airlines (SAS)

Apollo Extends Charter Contract with Scandinavian Airlines (SAS) Garuda Indonesia and Singapore Airlines Sign FFP and Revenue Sharing Agreements

Garuda Indonesia and Singapore Airlines Sign FFP and Revenue Sharing Agreements Mandarin Oriental Signs Fifth Luxury Hotel in Italy

Mandarin Oriental Signs Fifth Luxury Hotel in Italy Saudia Signs Firm Order for 105 Airbus Aircraft

Saudia Signs Firm Order for 105 Airbus Aircraft IHG Signs Three Resorts in Turks & Caicos

IHG Signs Three Resorts in Turks & Caicos Plaza Premium Appoints Dr. Syafrina Sharif as Global Head of ESG & Sustainability

Plaza Premium Appoints Dr. Syafrina Sharif as Global Head of ESG & Sustainability TFE Hotels Launches New Loyalty Program

TFE Hotels Launches New Loyalty Program The First Collection at Jumeirah Village Circle Joins Marriott's Tribute Portfolio

The First Collection at Jumeirah Village Circle Joins Marriott's Tribute Portfolio Korean Air Partners AWS for AI-Powered Contact Center

Korean Air Partners AWS for AI-Powered Contact Center GOLIAT Project to Explore Use of Liquid Hydrogen in Aviation

GOLIAT Project to Explore Use of Liquid Hydrogen in Aviation Singapore Airlines to Establish a Foundation

Singapore Airlines to Establish a Foundation High-Speed Fun in Denmark! HD Video Interview with Aarhus Sea Rangers

High-Speed Fun in Denmark! HD Video Interview with Aarhus Sea Rangers 16 Exclusive HD Video Interviews from Routes Europe 2024 in Aarhus, Denmark

16 Exclusive HD Video Interviews from Routes Europe 2024 in Aarhus, Denmark 9 Exclusive HD Video Interviews from Routes Asia 2024 in Langkawi, Malaysia

9 Exclusive HD Video Interviews from Routes Asia 2024 in Langkawi, Malaysia 9 Exclusive Video Interviews with VIPs at ASEAN Tourism Forum 2024 in Vientiane, Laos

9 Exclusive Video Interviews with VIPs at ASEAN Tourism Forum 2024 in Vientiane, Laos 8 NTO Press Conferences from the ASEAN Tourism Forum 2024 in Vientiane, Laos

8 NTO Press Conferences from the ASEAN Tourism Forum 2024 in Vientiane, Laos 13 Exclusive HD Video Interviews with VIPs at World Travel Market 2023 in London, England

13 Exclusive HD Video Interviews with VIPs at World Travel Market 2023 in London, England 5 HD Video Interviews from APG World Connect 2023 in Monaco, France

5 HD Video Interviews from APG World Connect 2023 in Monaco, France 15 Exclusive Videos from Routes World 2023 in Istanbul, Türkiye

15 Exclusive Videos from Routes World 2023 in Istanbul, Türkiye

- Interview with Alisa Phanthusak, MD, Tiffany's Show Pattaya, Thailand")

Central Poland - Interview with Robert Makowski, Commercial Director (CCO)")

, Southampton (SOU) and Aberdeen Airports (ABZ) - Interview with Christopher Tibbett, Aviation Director")

in Denmark - Interview with Lotta Sandsgaard, CEO, at Routes Europe 2024")

- Interview with Prof. Dr. Martin Roll, CEO, at Routes Europe 2024")

- Interview with Michiel Parent, Commercial Director")

- Interview with Marc Watkins, RDM")

in Estonia - Interview with Eero Pärgmäe Board Member and CCO")

- Interview with Gary Cobb, Airport Director")

in Western Australia - Interview with Stephanie Juszkiewicz, SVP Aviation Business Development, at Routes Asia 2024 in Langkawi, Malaysia")

Rayong / Pattaya, Thailand - Interview with Ampika Chadawong, at Routes Asia 2024 in Langkawi, Malaysia")

in Nha Trang, Vietnam - Interview with Le Thi Hong Minh at Routes Asia 2024 in Langkawi, Malaysia")

- Interview with Simon Miller, Senior Manager Market Intelligence, at Routes Asia 2024 in Langkawi, Malaysia")

at ATF 2024")

2024 in Vientiane, Laos")

to Rebrand as DTH Travel - HD Video Interview with Stephan Roemer, Partner and Group CEO")

- HD Video Interview with Rohan A. Khaunte, Minister for Tourism at WTMLDN 2023")

Tourism - Interview with Prateek Hira, President & CEO of Tornos, at WTMLDN 2023")

- Interview with Sheo Shekhar Shukla, Principal Secretary Culture & Tourism, at WTMLDN 2023")

- Interview with Dr. Rashmi Sharma, Director - Department of Tourism, at WTMLDN 2023")

2023")

.")

of Malaysia Tourism Promotion Board (MTPB), at Routes World 2023 in Istanbul, Türkiye.")

at Routes World 2023 in Istanbul, Türkiye.")

- Interview with Ulla Lettijeff, SVP and Director (Finavia), at Routes World 2023")

New Satellite Terminal - Airports of Thailand Interview with Paweena Jariyathitipong, Senior Executive Vice President (Engineering and Construction), by Steven Howard of TravelNewsAsia.com on 15 October 2023 at Routes World 2023 in Istanbul, Turkiye.")

- Interview with Qiang Wang, Deputy GM Aviation Business, at Routes World 2023")

in Kazakhstan - Exclusive Video Interview with Co-Founder, Auez Tulegenov")

")

, Hua Hin (หัวหิน), Prachuap Khiri Khan (ประจวบคีรีขันธ์), Cha-Am (ชะอำ) and Petchaburi (เพชรบุรี), to those living in Thailand as well as regional travellers and businesses.")

has been described as 'an important enabler of Sabre’s vision for personalized travel'. But what exactly is NDC, and what role does Sabre play in its development and future growth? Those are just two of the questions that Steven Howard of TravelNewsAsia.com asks Kathy Morgan, Vice President - Offer Sourcing at Sabre Travel Solutions.")

Conservation, Jungle Bubbles and Tourism in Thailand - Interview with John Roberts of the Golden Triangle Asian Elephant Foundation (GTAEF)")

- State of the Industry 2020 with Subhas Menon, Director General")

, Thailand's Deputy Prime Minister and the Minister of Public Health and Dr. Tanarak Plipat, Deputy Director General of Thailand's Department of Disease Control speaking at the World Health Organisation's (WHO) COVID19 virtual press conference on 6 November 2020")

does, as well as how the year 2019 ended and what they have planned for 2020. John tells us what Jungle Bubbles are, who is staying in them, how many elephants people can expect to see, whether they are safe, and how they plan to expand this rather unusual idea. All that and much, much more in the interview.")

2020. Filmed at TAT's office in London on 8 January 2020, Khun Chiravadee tells us when and where TTM+ 2020 will take place, why that city was chosen, what the theme will be this year, and how many buyers and sellers are expected to attend. Khun Chiravadee tells us how many buyers from the UK will be going and how those buyers will be chosen, and much, much more.")

. Yanik tells us how the certification levels within NDC, such as Level 4 and @scale, differ from one another, why they are important, what needs to be done to go from one level to another, and so very much more.")

in Bangkok, Steven Howard of TravelNewsAsia.com asks Robert to give us an update on the company, NDC, NGS and the industry in general.")

Yangsuksathaporn, General Manager of the Vince Hotel Bangkok Pratunam. In this interview, filmed in the rooftop bar of the hotel on 1 November 2019, Khun Fah tells us about the location of the Vince Hotel Bangkok Pratunam, where the hotel's guests are coming from, how 2019 compares to 2018, what its USPs are, where all the creative ideas come from, which other events the hotel will attend this year, what guests can expect from the property and what plans they have for 2020. All that and much, much more in the FHD video and podcast.")

, Siem Reap (REP) and Sihanouk (KOS), how this year compares to last year, and what expansion plans they have for the future.")

, the Group Director - Travel Industry for Cape & Kantary Hotels, to ask him about the event and the company's plans for the future. In this exclusive interview, filmed at the Cape Panwa Hotel on 21 July 2019, Khun Tom tells us about three new properties the hotel group plans to open in the next few years, how they will be branded, where they will be located, and how many rooms each will have.")

and has attended the last nine, including the most recent edition in Jomtien, Pattaya last week. In this exclusive interview, filmed on the first day of TTM+ 2019, Kati Hakkinen explains where Khanom is in Thailand, what its attraction is and what is the best way to travel there.")

2019 in Pattaya. Steven Howard of TravelNewsAsia.com sat down with Khun Sillapat Watcharapong, Director of Marketing at the Racha Kiri Resort in Khanom, to ask him about his resort and Khanom as a destination.")

2019, held in Jomtien, Pattaya last week, not only had the crucial buyers meet sellers component, but also different workshops with expert speakers sharing their knowledge with media and sellers alike. One such expert, Khun Arrut Navaraj, Managing Director of Suan Sampran, gave an interesting talk to delegates about Organic Farming and Sustainable Tourism.")

in Pattaya. Mr. Tanes Petsuwan, TAT's Deputy Governor for Marketing Communications, used the media briefing to outline their plans for 2019 and beyond, and give some insight into which of Thailand's less well known destinations they will be promoting and how. This video includes the Q&A at the end.")

, in Halong, Vietnam on 26 May 2019.")

as Miss USA. In this interview, filmed on 7 March 2019, Steven Howard asks Jazell why she has come so far to compete and why she chose Miss International Queen above all the others.")

, Managing Director of Phuket-based Sky Marine Group. In this interview, filmed at the Ocean Marina Pattaya Boat Show on 2 December 2018, Steven Howard asks Khun Thanaya about her business which includes yacht sales, hull cleaning and maintenance, as well as luxury yacht charters.")

Song, Managing Vice President Passenger Network & Sales about the airline and its plans for the future.")

62nd Assembly of Presidents.")

and Sustainable Tourism - PHIST Interview. What could the World Wide Fund for Nature, or WWF as it is more commonly known, possibly have in common with the hotel industry? In this exclusive interview with Maggie Lee, Market Transformation Manager at WWF Singapore, we ask Maggie about this, and much more.")

season and the peak November - May season.")

forum which was held at the resort on 24 September.")

in London.")

at Farnborough Airshow 2018 on 16 July, Steven Howard of TravelNewsAsia.com asks Mr. Gauss about the aircraft, why it is so popular, what makes it special and what plans they have for future orders.")

Province, Thailand.")